| Social Housing RMI Business Intelligence |

|

| Back once again for the renegade master. |

| This month marks a significant step forward in how clients interact with Locarla, with improvements across both data insight and day‐to‐day usability. |

| We’ve introduced the new Daily Bulletin format, designed to surface more relevant opportunities with clearer structure and faster scanning. Alongside this, our RAG capability now includes the Locarla Retrofit Priority Index (LRPI) ‐ a major enhancement that moves analysis beyond raw EPC data into prioritised, decision-ready insight. This is supported by the latest Retrofit Report, giving a deeper, more structured view of retrofit demand across the sector. |

| Further updates are imminent. On the 27th, or as near as damn it, we’re releasing a redesigned contract interface that brings all notice types into a single, unified view. This includes simplified bulletin setup, improved filtering, and new visual indicators such as notice-type and timing “pills” (including published date and submission deadline) to make opportunity assessment quicker and more intuitive. |

| In parallel, we are improving how tenders are selected and delivered to you. Instead of relying on rigid trade filters, we are developing a more intelligent approach that understands what you’re actually looking for ‐ meaning you can describe opportunities in plain English and receive far more relevant results. Early testing is already showing a noticeable improvement in accuracy. |

| On with the show, we hope you enjoy it, and if you’re in Brighton for the CIH conference look out for Amy and the performing monkey she takes with her. |

| ‘Blue links‘ for all and ‘green links‘ are behind login, so dependent on your licence. |

| Welcome, welcome, one and all. |

|

|

| Regional Retrofit Demand ‐ Improvement Insights |

|

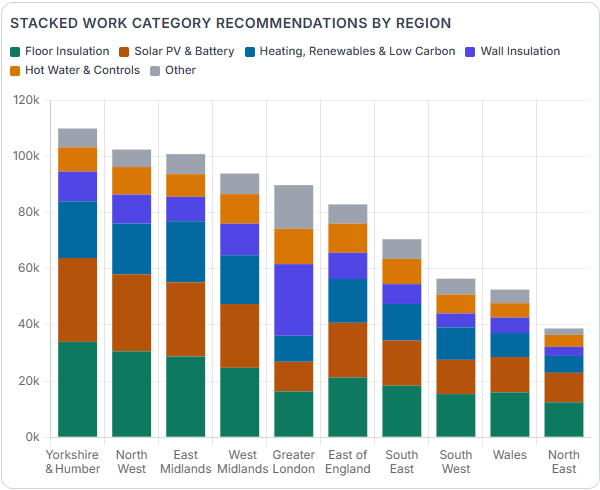

| Retrofit demand is not just about volume ‐ it’s about the type of work dominating each region. |

| The chart below shows how improvement recommendations are distributed across England and Wales. While Yorkshire and the North West carry the largest overall pipelines, the structure of that demand is consistent: floor insulation and solar PV appear most frequently, often on the same properties. |

| London stands apart. Its profile is driven by wall insulation at a significantly higher rate than any other region, reflecting the capital’s concentration of older, solid-wall housing stock and the constraints of dense, urban environments. |

| This is a snapshot of our wider Retrofit Intelligence dataset, where demand can be explored in detail by landlord, location and work type – supporting more targeted bid and growth strategies. |

| If you are one of our Retrofit & Decarbonisation clients, you will be receiving a link to access the full report later today. |

|

|

|

|

| It’s all News to me! |

|

|

|

| FUNDING & INVESTMENT |

|

Guinness seals £1bn long-term maintenance deals

The Guinness Partnership signs 15‐year contracts with Axis Europe, Fortem Solutions and partners to upgrade and decarbonise 70,000 homes.

Source → |

|

Rotherham approves £312.6m housing upgrade and expansion plan

Rotherham Council to upgrade thousands of homes, boost energy efficiency and deliver new housing over four years.

Source → |

|

Powys approves £270m council housing investment plan

Powys County Council to build 350+ homes and upgrade existing stock, boosting quality and energy efficiency over five years.

Source → |

|

BCP approves £122m council housing upgrade plan

Bournemouth, Christchurch and Poole Council to improve homes with repairs, upgrades and energy efficiency measures targeting EPC band C by 2030.

Source → |

| PROCUREMENT & PIPELINE |

|

£120bn government construction framework tender launched

Crown Commercial Service opens bidding for eight‐year framework supporting local authorities, housing providers, NHS bodies and emergency services from 2027 to 2035.

Source → |

|

SNG appoints contractors to affordable homes framework

Sovereign Network Group appoints multiple partners to deliver its £10.9bn housing and regeneration programme across regions.

Source → |

|

LCP appoints 44 firms to £3bn construction framework

London Construction Programme names contractors including Galliford Try and Graham for five‐year works covering build, retrofit and repairs.

Source → |

|

Moray launches maintenance framework for local contractors

Moray Council invites bids for four‐year framework covering repairs and maintenance across 6,400 homes and 29 trade lots.

Source → |

| DELIVERY & RETROFIT |

|

Sureserve wins Ayrshire repairs contract trio

Sureserve Energy Services secures five‐year reactive maintenance deal with Ayrshire Housing, Shire Housing Association and Atrium Homes.

Source → |

|

WPS lands role on £480m national decarbonisation framework

WPS appointed to Procurement Hub framework to deliver retrofit and energy upgrades across homes in England.

Source → |

|

London launches new Warm Homes retrofit delivery model

Greater London Authority invites bids via Procure Plus for six‐contractor model to boost retrofit delivery across London.

Source → |

|

|

| Locarla Retrofit Priority Index (LRPI) |

|

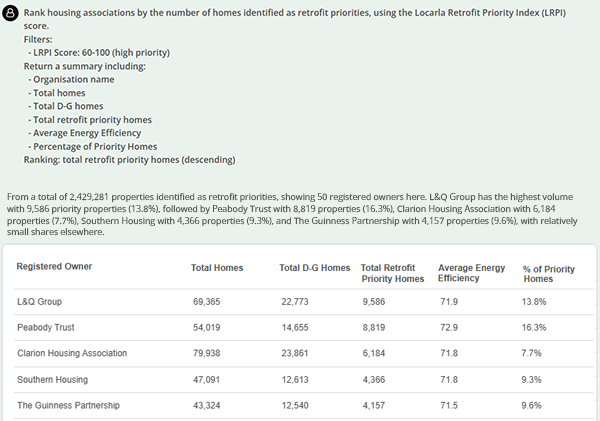

Using LRPI, we can move beyond broad EPC-based assumptions and quantify retrofit need at organisation level. The example below ranks housing associations by the volume of high-priority homes (LRPI 60–100), providing a clearer view of where demand is most concentrated.

What stands out is not just scale, but variation ‐ organisations with similar stock sizes can have materially different retrofit exposure. This allows contractors and suppliers to prioritise clients based on actual need, while housing providers can benchmark their position against peers using consistent, property-level data. |

|

Targeting (Commercial Use Case)

“Which housing associations in the North West have the highest volume of high-priority retrofit homes (LRPI 60–100), and what proportion of their stock does this represent?” |

Portfolio Risk / Exposure (Client Insight)

“For the top 20 housing associations by stock size, how does the percentage of LRPI high-priority homes compare, and which organisations are above the national average?” |

Work Type Planning (Operational Insight)

“Break down high-priority LRPI homes by property type and construction age band for London-based housing associations.” |

| Good LRPI prompts always include at least two of the following: |

| • |

Where (region / LA) |

| • |

Who (organisation / type) |

| • |

How much (volume + %) |

| • |

What type (property / age / archetype) |

|

LRPI in the RAG is included as part of the Retrofit & Decarbonisation licence – if this is you click here https://www.locarla.ai/chat

If you’re a client and want to upgrade – speak to Amy amy.fitt@locarla.com

Not yet a client? Amy can help you with that too. |

|

| Show me the money! |

| A PDF guide to contract management on Locarla. |

|

|

| PROCUREMENT PIPELINE OVERVIEW |

| Procurement activity continues to progress ‒ with opportunities emerging across development, planned works, repairs, and compliance in the UK social housing sector. |

|

| TOP OPPORTUNITIES |

Wirral Council ‐ PIN ‐ National Developer Framework (Questionnaire Submission by 29.04.2026)

National developer framework covering development agreements, joint ventures, and feasibility services across England. |

England|£12bn| England|£12bn| 21 days 21 days |

| → View notice | View client |

|

Community Housing ‐ Planned Works Framework ‐ 1362

Multi‐supplier framework covering planned, cyclical, and improvement works across housing and building assets. |

| UK Wide|£1.6bn|43 days |

| → View notice | View client |

|

Portsmouth City Council ‐ Term Service Contracts for the Repairs & Maintenance of Residential and Commercial Properties for Council Managed Assets ‐ 2026

Deliver repairs and maintenance services for housing stock and corporate assets across three lots. |

| South East|£765m|17 days |

| → View notice | View client |

|

Platform Housing Limited ‐ Strategic Asset Management Programme – Lot 1 – Home Investment & Retrofit

Home investment, retrofit, energy efficiency, and planned capital works across housing stock. |

| East Midlands, West Midlands, East Anglia, South West|£672m|16 days |

| → View notice | View client |

|

| REPAIRS & MAINTENANCE |

Westminster London Borough ‐ Housing Responsive Repairs and Major Works Contracts

Responsive repairs, voids, and major works for housing stock across two lots. |

| Greater London|£746m|27 Days |

| → View notice | View client |

|

Platform Housing Limited ‐ Complex Repairs and Major Voids

Complex repairs and major void works across housing stock in three regional areas. |

East Midlands, West Midlands|£144m|16 Days |

| → View notice | View client |

|

Hammersmith & Fulham London Borough ‐ Housing Repairs 2027

The Council is tendering housing repairs and maintenance services, including voids, lifecycle works, and kitchen, roofing, and damp improvements. |

| Greater London|£118.5m|24 Days |

| → View notice | View client |

|

Sunderland City Council ‐ Minor Works Framework

Minor works framework covering 41 lots across trades including electrical, roofing, and gas. |

| North East|£50.9m|24 Days |

| → View notice | View client |

|

Progress Housing Group ‐ DLO Support

Provide DLO support for specialist repairs and maintenance across various housing trades. |

| England|£-|24 Days |

| → View notice | View client |

|

| PLANNED WORKS, REFURBISHMENT & RETROFIT |

South East Consortium ‐ Capital Works Framework

Capital works framework covering kitchens, bathrooms, roofing, electrical, and cyclical decorations. |

| UK Wide|£250m|35 Days |

| → View notice | View client |

|

Amplius ‐ Provision of the Supply and Installation of Planned Kitchen and Bathroom Refurbishments and Associated Works

Supply and installation of planned kitchen and bathroom refurbishments and associated works. |

| Yorkshire and the Humber, East Midlands, West Midlands, East Anglia|£96.8m|17 Days |

| → View notice | View client |

|

Ashfield District Council ‐ Housing Refurbishment Contract to Various Council Owned Properties

Housing refurbishment works across various council-owned properties. |

| East Midlands|£69m|3 Days |

| → View notice | View client |

|

L&Q Group ‐ Kitchens Supply & Supply & Fit

Multi‐lot kitchen framework launching shortly, ensuring value, quality, and delivery, with defined single-supplier, primary, and contingency supplier arrangements. |

| Greater London, South East, North West, East Anglia, West Midlands|£40m|– |

| → View notice | View client |

|

PA Housing Ltd ‐ Windows and Doors Long Term Contracts ‐ PR-11056‐PA

Window and door replacements across housing stock in London and the South East. |

| Greater London, South East|£27.9m|14 Days |

| → View notice | View client |

|

| COMPLIANCE & SAFETY WORKS |

Platform Housing Limited ‐ Passive Fire Protection Works

Passive fire protection works including fire stopping, compartmentation, and fire doors across housing stock. |

| East Midlands, West Midlands|£120m|3 Days |

| → View notice | View client |

|

Portsmouth City Council ‐ PIN ‐ Building Safety Higher Risk Buildings Framework (Site Visits from 27.04.2026 to 15.05.2026)

Building safety framework covering fire stopping, fire doors, sprinklers, and evacuation systems. |

| South East|£120m|45 Days |

| → View notice | View client |

|

Islington London Borough ‐ Domestic Gas and Ad hoc Non-domestic Boiler Installations, Servicing and Repairs

A new framework for the delivery of domestic gas boiler servicing, repairs, and installations across its housing stock. |

| Greater London|£78.5m|20 Days |

| → View notice | View client |

|

Platform Housing Limited ‐ Mould Surveys, Cleans and Remedial Works

Mould surveys, cleaning, and remedial works across housing stock in three regional areas. |

| East Midlands, West Midlands|£48m|16 Days |

| → View notice | View client |

|

Platform Housing Limited ‐ Electrical Testing and Repairs ‐ Lot 3

Electrical condition reports, remedial works, and repairs across housing stock in three regions. |

| East Midlands, West Midlands|£42m|3 Days |

| → View notice | View client |

|

Edinburgh City Council ‐ Gas Engineering Works Framework Agreement ‐ CT1662

Gas engineering works framework covering installation, replacement, maintenance, and servicing across four lots. |

| Scotland|£13.6m|31 Days |

| → View notice | View client |

|

| NEW-BUILD & DEVELOPMENT |

Islington London Borough ‐ New Homes Housing Partnerships ‐ 2526-0569

Deliver a multi-site new homes housing portfolio funded through land value. |

| Greater London|£416.6m|3 Days |

| → View notice | View client |

|

|

| The Other League Tables |

|

| Along with our main monthly league tables, ❲see below❳, we also produce tables based on the following trades: Retrofit, Asbestos Survey, Fire Risk Assessment, Water/Legionella & Stock Condition Survey. ❲Premium Clients, click here for the PDF❳ |

| Top of the league in each table are …. |

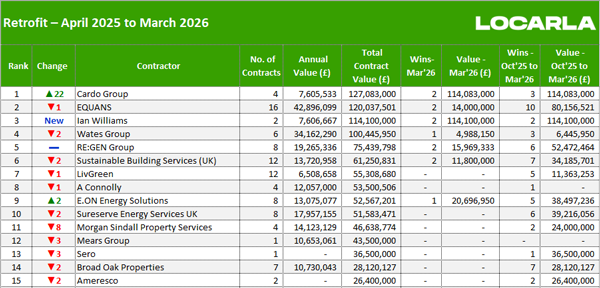

| Retrofit: |

| Cardo Group |

| Asbestos Survey: |

| Tersus Consultancy |

| Fire Risk Assessment: |

| IFI Group |

| Stock Condition Surveys: |

| Pennington Choices |

| Water / Legionella: |

| Sureserve Compliance Water |

|

|

| March League Tables |

|

|

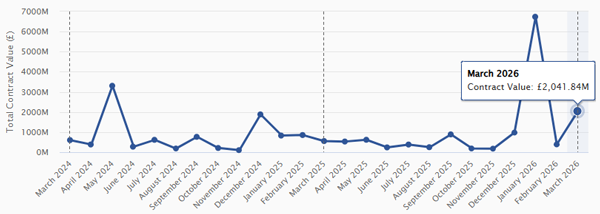

| Built Environment Contracts ‐ March 2026 Overview |

| March shows a highly uneven distribution of contract value, driven by a small number of large awards rather than broad market activity. Total value reached £2.04bn, but this sits alongside relatively modest activity across several core workstreams.

The key takeaway is concentration, not consistency – a recurring theme where monthly totals are increasingly shaped by episodic, high-value releases rather than steady pipelines.

At contractor level, no single firm dominates across all trades, reinforcing a fragmented delivery landscape where capability remains trade-specific. |

|

| Top Contractors (Showing 10 of 50 companies) |

|

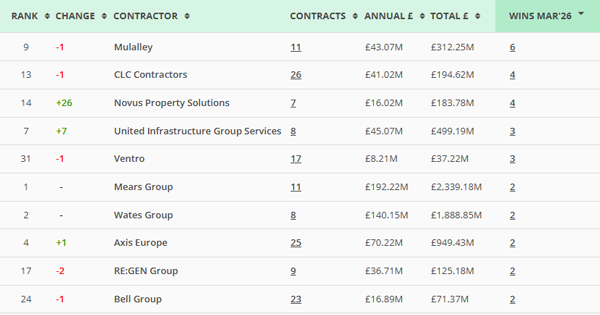

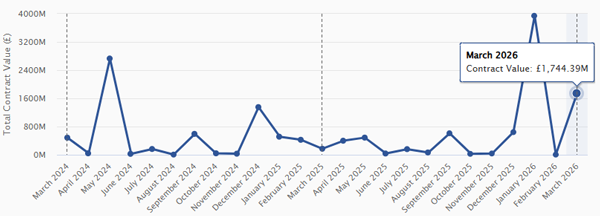

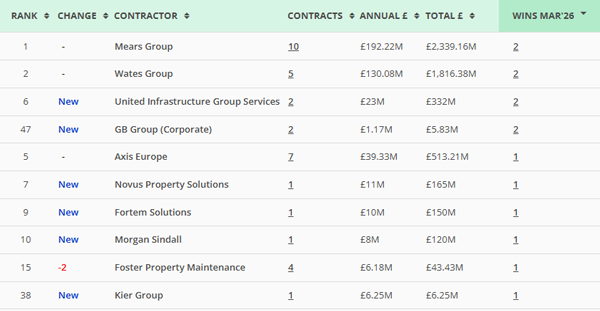

| Responsive Repairs |

| March delivered £1.74bn, one of the strongest months in the past year, but the underlying pattern remains volatile. |

| • |

Mears Group and Wates Group continue to anchor the sector, combining scale with repeat frameworks. |

| • |

The appearance of United Infrastructure Group Services as a new entrant signals framework churn rather than organic growth. |

| • |

A long tail of single-award contractors highlights low barriers to entry at lower contract values, but limited upward mobility. |

|

Interpretation:

This is a framework-led market, not a competitive open market. Winning position is defined by being on the right frameworks, not bidding volume. |

|

| Responsive Repairs (Showing 10 of 95 companies) |

|

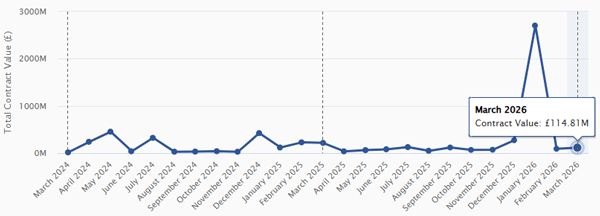

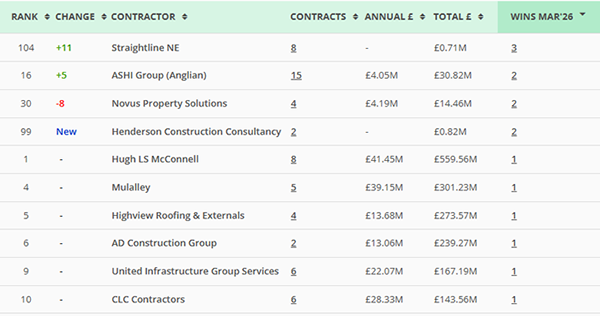

| Planned Works (Kitchens, Bathrooms, Windows & Doors) |

| Despite a visible spike earlier in the year, March activity is relatively subdued at £114.8m. |

| • |

Mulalley and Hugh L S McConnell maintain steady presence, reflecting long-term programme delivery rather than new wins. |

| • |

New and lower-ranked entrants picking up multiple wins suggests regional or lot-based packaging of work. |

|

Interpretation:

This is a programme-driven market, where visibility comes from pipeline continuity, not monthly spikes. |

|

| Planned Works (Showing 10 of 185 companies) |

|

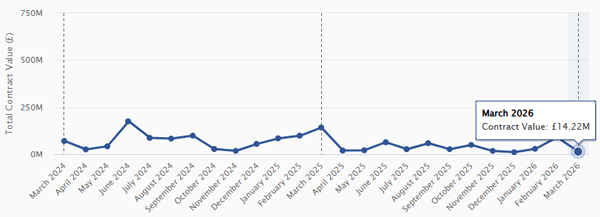

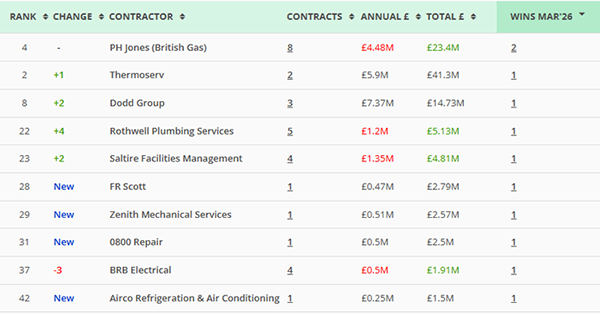

| Gas Servicing & Central Heating |

| At £14.2m, March is relatively quiet compared to prior peaks. |

| • |

PH Jones remains structurally dominant, but contract values are modest. |

| • |

The spread of smaller wins across providers like Thermoserv and Dodd Group indicates high fragmentation. |

|

Interpretation:

This is a high-frequency, low-value market. Scale comes from aggregation over time, not individual contract wins. |

|

| Gas Servicing & Central Heating (Showing 10 of 95 companies) |

|

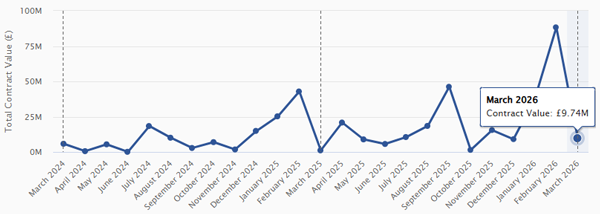

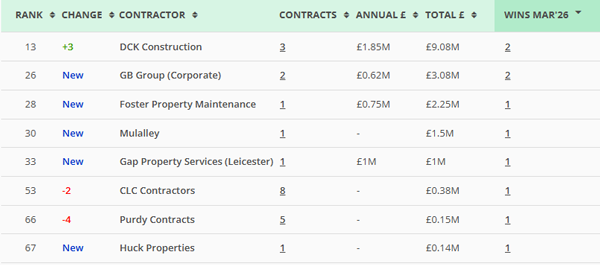

| Voids |

| March sits at £9.74m, but the wider trend shows sharp peaks and troughs. |

| • |

Contractors such as DCK Construction and GB Group appearing with multiple wins suggests short-cycle, reactive procurement. |

| • |

Limited repeat dominance points to operational rather than strategic contracting. |

|

Interpretation:

Voids is a reactive market, closely tied to housing turnover and internal pressures rather than long-term planning. |

|

| Voids (Showing 8 of 88 companies) |

|

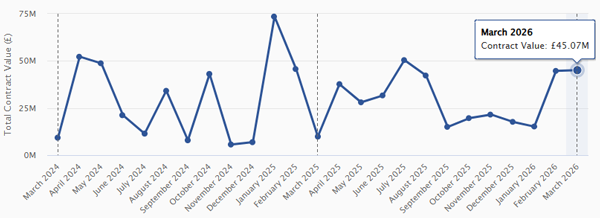

| Fire Safety |

| March records £45.07m, continuing a steady recovery from earlier volatility. |

| • |

Mulalley and Ventro remain consistent performers. |

| • |

Increased activity from compliance-led specialists such as Sureserve Compliance Fire reflects regulatory-driven demand. |

|

Interpretation:

This is a compliance-driven market, where demand is non-discretionary and less sensitive to budget cycles. |

|

| Fire Safety (Showing 10 of 157 companies) |

|

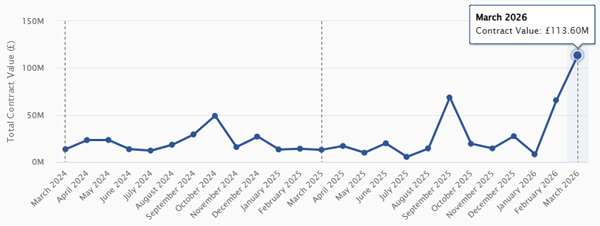

| Roofing |

| March shows a significant uplift to £113.6m, driven by a late-month surge. |

| • |

Specialised Group and Jennings Roofing lead in volume of wins rather than value. |

| • |

The presence of smaller contractors with multiple wins indicates regional contract packaging and specialist procurement routes. |

|

Interpretation:

Roofing sits between planned and reactive works – a hybrid market influenced by both capital programmes and urgent repairs. |

|

| Roofing (Showing 10 of 136 companies) |

|

What This Means (Cross‐Market View)

Across all trades, three structural patterns emerge: |

1. Concentration of Value

Monthly totals are increasingly driven by a handful of large awards, not broad-based activity.

2. Framework Dependency

Repeat winners dominate because of framework positioning, not because they win more competitions month-to-month.

3. Trade Fragmentation

There is no universal contractor dominance ‐ leadership is trade-specific, reinforcing the need for targeted bidding strategies. |

|

| The market is not short of opportunity ‐ but it is highly structured. Success depends less on finding tenders, and more on understanding where contract value is actually concentrating. |

| RMI Insight & Decarbonisation clients can view the full dynamic league tables here. |

|

| Reports, Reports & more Reports. |

| All our RMI Insight & Decarbonisation clients receive news, reports, contract data and LA Minutes every day. |

|

|

|

| Pension Insurance Corporation |

Housing Ombudsman Service |

Chartered Institute of Housing |

|

|

|

|

| London Gov.UK |

Fabian Society |

S&P Global |

|

|

|

|

| Office for National Statistics |

GOV.UK |

GOV.UK |

|

|

|

|

| Plumbing & Heating Merchant Index |

Builders Merchant Building Index |

The Scottish Government |

|

|

|

|

| Federation of Master Builders |

Home Builders Federation |

National Audit Office |

|